When the analytics chief at Whoop looked across his company’s tech stack recently, he noticed something quite interesting – every tool, vendor, or platform they use now has their own AI agent. Slack has one, Snowflake has one, Google Workspace has one. Even other software companies that weren’t competing in the AI space before are now all fighting for the exact same slice of attention from customers.

And that’s painted the story we’ve seen across 2024-2025. Every enterprise software company is building near-identical agents that act as assistants who comb through data, forecast sales, triage IT tickets, analyze customer messages, or even write code for you. Subsequently, this has resulted in an explosion of choice – and a lot of overlap – that’s left many buyers frozen in place.

It’s also created a surprisingly tricky situation for Salesforce as well. Agentforce has been coined as the defining product of the enterprise AI era, but the reality is that the CRM giant is battling competitors on all sides. On top of that, adoption has been slower than expected, and they now must prepare for a highly-awaited Q3 earnings call where Wall Street will want proof that agents can actually move the needle.

So for Salesforce, this has become more than just a competitive battle with familiar foes. It’s a story about what happens when everyone looks the same, and whether Salesforce’s long-held advantage with customer data is strong enough to cut through the noise.

The Agent Market Has Become Crowded and Confusing

If you look back to around a year ago, the newly introduced concept of an AI agent inside enterprise software was exciting, even if it did raise concerns around security and performance. But it’s safe to say that the space has become overwhelming just as quickly.

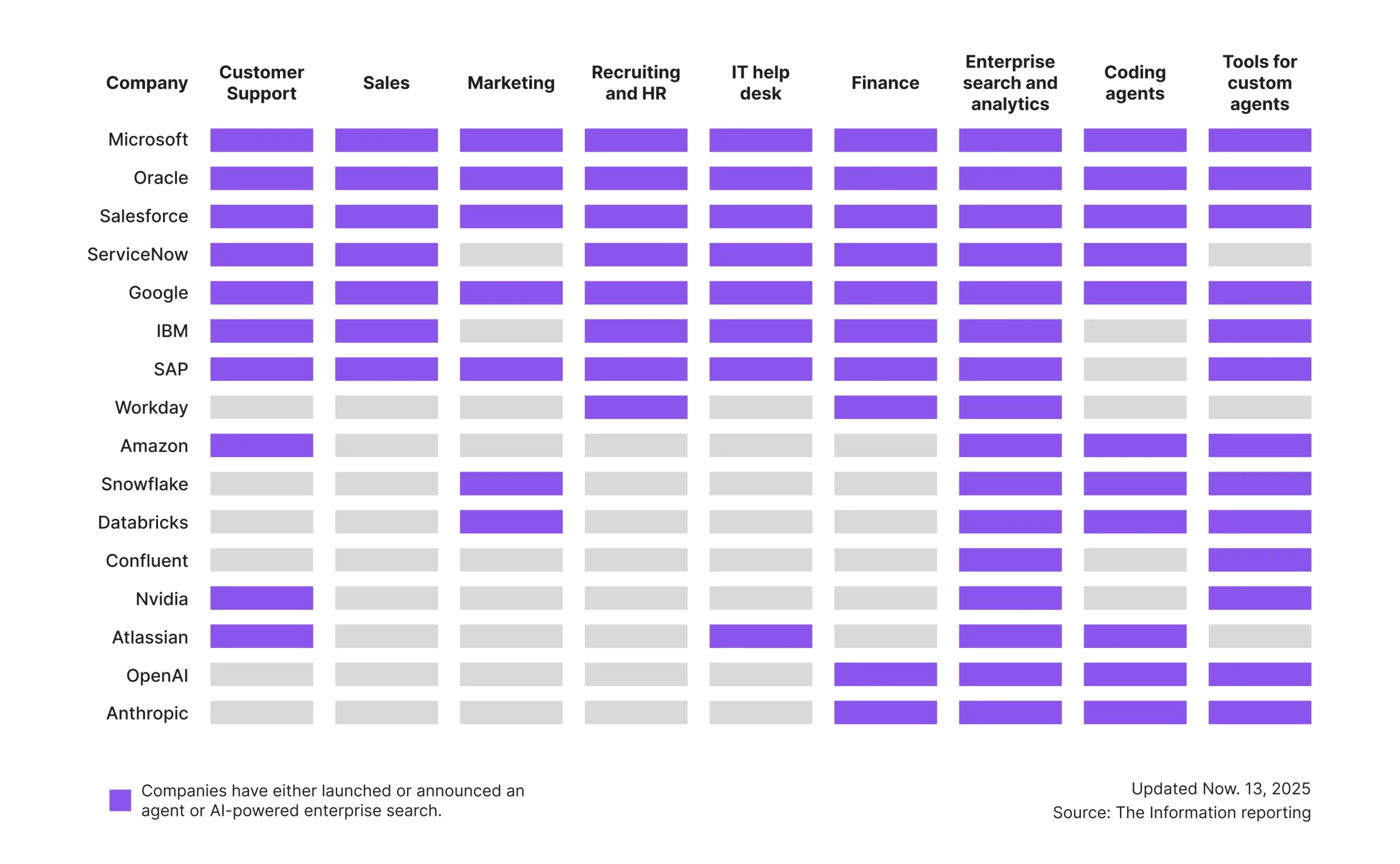

The clearest way to understand the current agent landscape is to look at the grid below, originally curated by The Information. The chart illustrates exactly what buyers have been feeling for a while now – nearly every major enterprise software company offers agents across multiple business functions, and most of them overlap in several areas.

Microsoft, Google, IBM, SAP, and Salesforce light up almost every category, from customer support to sales, finance, enterprise search, and coding agents. Companies that once stayed in their own lanes have had those barriers flattened by AI overnight.

Even traditionally specialized companies like ServiceNow, Databricks, Confluent, and NVIDIA are now ticking AI boxes that are well out of their traditional remit. Meanwhile, AI native players like OpenAI and Anthropic sit across the entire grid as their underlying model can be adapted to all potential categories.

So in turn, the market has become so crowded that enterprises are pausing any decisions as the landscape has become incoherent. Ryan Teeples, Chief Strategy Officer at 1-800Accountant, told The Information that the overlap makes the selection process “extremely difficult” and that many companies are choosing to wait until winners emerge.

The “pause until clarity” approach is important, and directly feeds into Salesforce’s current adoption issues. The ecosystem is already generally uncertain about aspects such as pricing, ROI, and the setup process. Add in the plethora of lookalike competitors, and the hesitation will only continue.

Salesforce’s Long-Term Advantage

While Salesforce may be facing continuous challenges in the agent market, it has a key structural advantage over many of its competitors – the vast amounts of data on its side.

Salesforce customers store years or even decades of deeply structured information in Sales Cloud, Service Cloud, Marketing Cloud, and increasingly in Data 360 (formerly Data Cloud). This is exactly what a typical AI agent needs to perform high-value tasks, and it’s notoriously difficult to move between systems.

Customers like Adecco illustrate this, saying: “It’s very simple. If we have the data stored in Salesforce, we use Salesforce.” This gravitational pull is real, and it’s why Salesforce-native agents can still succeed – even if adoption is slow at the moment.

It’s also worth considering how important Slack is to Salesforce’s edge. As a distribution channel, the overlap between Agentforce and Slack AI makes Salesforce one of the few companies with both the data and the daily workflow interface to deploy agents at scale.

So the long-term picture might not be as bleak as the early adoption narrative suggests.

Salesforce’s Adoption Problem Is Not About the Software…

If we zoom out for a minute, it becomes clear that slow agent adoption is more of an enterprise problem than a Salesforce problem. While startups can roll out agents practically overnight, Fortune 500 companies move at a much slower rate. They’ll want to run pilots, hold workshops, and need extensive help to clean their data and connect their systems. And often, they probably won’t buy until their peers do first.

So, yes, Agentforce adoption is slower than hoped – but that’s true for the whole tech ecosystem, not just Agentforce.

The specific problem Salesforce faces is that it has tied its entire future to the agentic narrative. They’ve talked about Agentforce as a key growth pillar, the thing that will push them into their next chapter. And because of that, there’s more pressure on them to show quick, visible wins. As Q3 approaches, investors want proof that these agents aren’t just a slick Dreamforce demo and that real companies are getting real value out of them.

That’s why adoption matters. Not because Agentforce is struggling behind the scenes, but because the market needs more evidence, more stories, and more clarity.

If Salesforce can tighten the narrative, simplify adoption, and double down on its data advantage, it has everything it needs to win. Not because it has the flashiest agent demos, but because it has the deepest, richest, most valuable data foundation in the enterprise. In the end, that’s what will matter most amidst this broad competitive space.

Final Thoughts

The agent enterprise market is chaotic, crowded, and, in many cases, very confusing.

Buyers are paralyzed, and competitors are gaining early attention, so the pressure is on Salesforce more than ever to prove Agentforce is more than just a collection of demos.

However, the long-term advantages are very much on Salesforce’s side – they have the data, the distribution, the ecosystem.

The question now is whether Salesforce can move fast enough and communicate clearly enough to turn those advantages into adoption before the market consolidates. Because in a world where everyone sells the same exact agent, the company that controls the data layer has the best chance of winning. And Salesforce still has every opportunity to be that company.